Using Collars to Protect Over Earnings

Has this market been on a wild ride or what? As an investor, your heart has probably been in your throat several times with the feeling the market is going to take another big downturn. Selling a call to help finance a long protective put has not been a bad idea over the past couple of months. Generally, collars are used by investors for this exact situation. But many investors fail to realize what collars can do to protect their equity position at any time and especially over what could be a volatile earnings announcement. We are smack dab in the middle of quarterly earnings and with the economy in potentially bad shape, now might be as good as time as any to discuss this somewhat simple, but effective option strategy yet again.

Collar Basics

An option collar is holding shares of stock and buying a put and selling a call on the same underlying. Usually both the call and the put are out-of-the money when establishing this option combination. One collar represents one long put and one short call along with 100 shares of the underlying stock. One of the main objectives of a collar is to protect the shares of stock from decreasing in value rather than increasing returns.

At the time of this writing, Tesla Inc. (TSLA) was expected to announce earnings the following week. If an investor is trying to protect his or her stock position from a gap lower after the announcement, a collar could be considered. Selling a call option limits the gains if the stock gaps higher rather than lower similar to how a covered call would limit gains on a stock position. But a collar is done in order to pay for some if not all of the long put’s premium. As I like to say, there are always trade-offs with options trading.

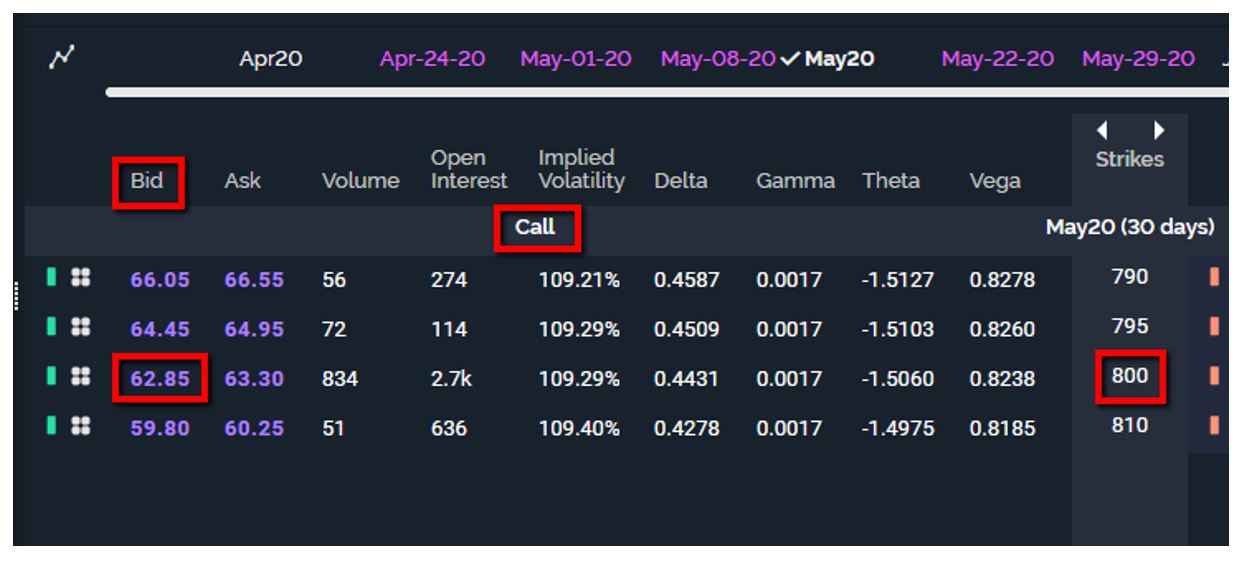

Take a look below at the chart of TSLA. In mid-April, the stock had been on quite the run higher. At the time, TSLA was trading at around $729.

A May (May 15th) 800 call can be sold for around 62.85, which can be used to purchase a May 665 put for around 62.10.

Calls

Puts

The sold call pays for the long put and the position protects the stock from further losses below the $665 level without any additional cost (actually a small credit) minus commissions. The 665 long put gives the owner the right to sell the stock at $665 until May expiration. The trade-off is if the stock gaps above $800, the 100 shares will be called away at $800 because they will expire in-the-money (ITM) and be automatically assigned if the short call is not bought back before expiration. If assigned, your long 100 shares will be sold at $800 regardless of how high they are trading at expiration.

Collars don’t always make sense but when an earnings report could lead to a potentially sizable gap lower, an investor should consider the alternatives -- which could be potentially much worse. Good luck!

John Kmiecik, Market Taker Mentoring