Calendar Spreads Ooze Positive Theta

Long calls and long puts cannot produce positive theta no matter how hard they try. For other option strategies, positive theta is the key component to a potentially profitable outcome. Long calendar spreads are certainly one of those option strategies. Let’s take a closer look.

A long calendar involves selling a call or put and buying the same strike call or put with a longer expiration. This position can have a positive, negative or essentially neutral delta depending on where the stock is trading in regard to the short strike. Unless it is a really directional calendar, potential success (profit) comes from positive theta. The short strike will have a bigger theta (which is positive) than the long strike (which is negative theta).

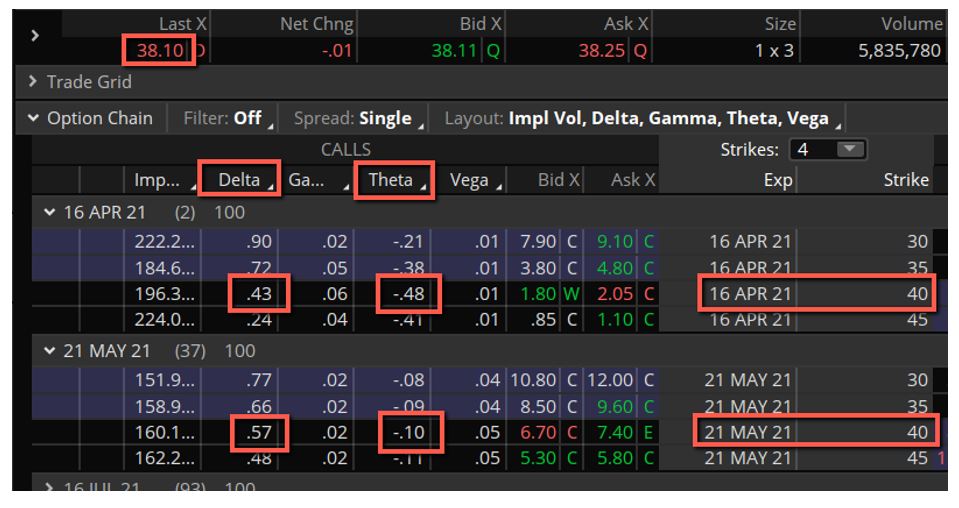

As time passes, positive theta can increase the spread’s premium, which is a good thing for a debit spread like a long calendar. But it can offset some delta risk too if the underlying moves away from the strike price. Take a look at the long calendar spread below.

The 40 call is sold and the following month’s 40 call is bought. The delta is about +0.14 (+0.57 - 0.43) with the stock currently trading at $38.10. The best-case scenario for this trade is for the underlying to move up to the $40 level as close to short expiration as possible. Positive theta for the position of 0.38 (+0.48 – 0.10) is the key.

With the current positive theta at 0.38, time passing would increase the spread’s premium by about $38 a day. If the stock moves higher or lower, delta will become more positive or turn negative if the underlying moves above $40. But because of the positive theta, it can offset some of the delta risk. In a market like we have seen, this is possibly invaluable.

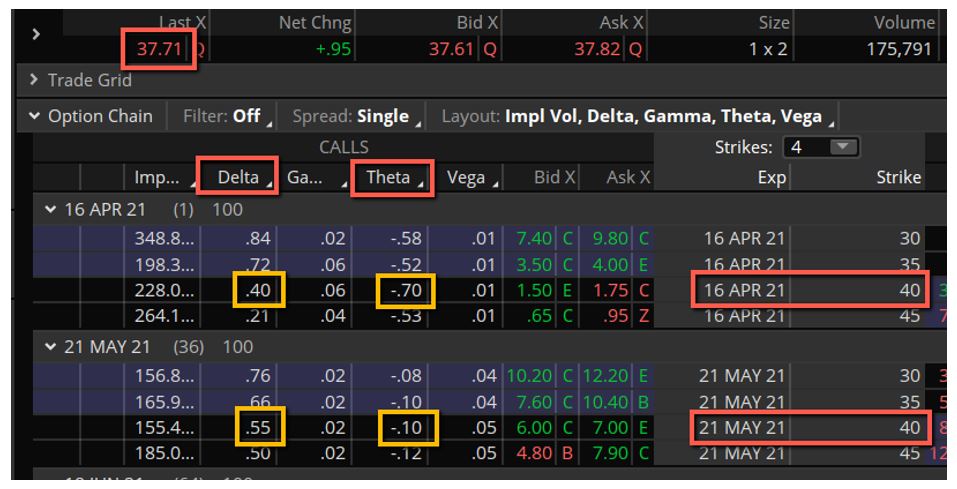

Fast forward one day.

The stock has not cooperated and has dropped almost $0.40. Delta is a tad more positive because of the drop in price, but checkout the positive theta. It has ballooned from about +0.38 to +0.60 (0.70 – 0.10). Not only is that bigger positive theta offsetting your delta risk, especially with the stock drifting a tad farther away from the $40 level where max profit can be achieved, it is increasing the spread’s premium, which could lead to an eventual profit.

A long calendar spread cannot perform miracles. Positive theta can only do so much to offset delta risk. If the stock moves far away from the short strike, delta will grow in the opposite direction that the stock is moving and positive theta (which will start diminishing) will not be able to offset the delta loss. But if the stock hangs in the general area of the short strike, positive theta will be your best friend, as it should be.

John Kmiecik, Market Taker Mentoring