Have You Checked Your Option Vega?

Implied volatility (IV) can be a huge influence on your option trades especially on single-leg trades. Keeping it simple, IV is used to determine the current price of option contracts together with other factors like time to expiration and the strike price. In general, when IV rises, so do option prices and when IV falls, so do option prices.

How IV Changes

Implied volatility levels generally increase when the market is bearish and decrease when the market is neutral or bullish as we have seen. Long options, both calls and puts, have positive vega because a rise in IV would increase the premium, which is good for a debit position. Short options, both calls and puts, have negative vega because a drop in IV would lower the premium, which is good for a credit position.

Option Vega

Vega changes the option premium for every 1% IV changes. If IV rises, so do call and put premiums and vice versa. So, when an option is bought, an option trader prefers IV to increase as mentioned above. An increase in option premium could lead to a profit to sell the option for more than what was paid, all other variables held constant. Of course, an option trader does not want IV to decrease after the option is purchased. Let’s take a quick look at a situation where that might happen.

Long Call Example

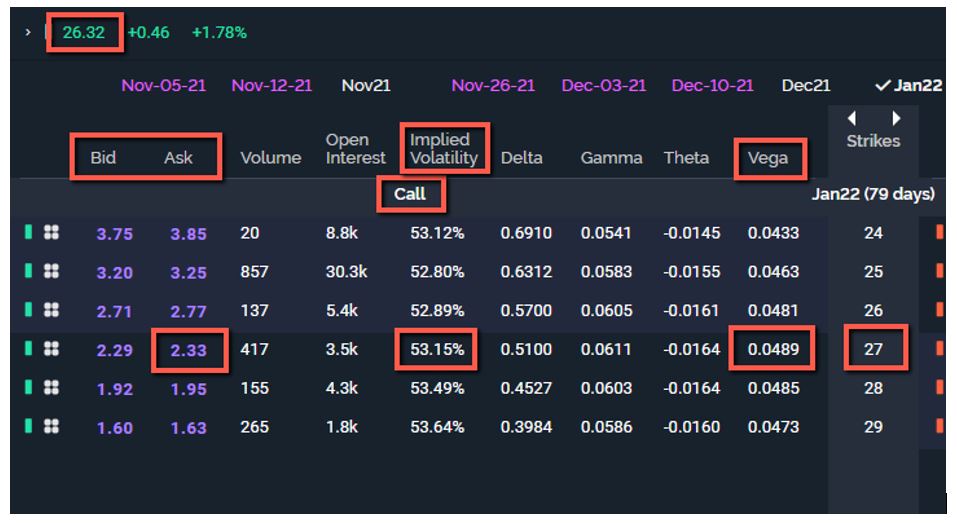

Suppose the market and a stock you are watching turn bearish and trade lower over several sessions. Most likely the IV would increase as the market and the stock you are watching move lower. After several down days, the stock drops to support and looks like it wants to move higher again. You purchase a long call as in the example below. The 27 strike call costs 2.33 ($233) and has a positive vega of around 0.05.

After moving lower, IV will most likely increase. Now, if the stock starts to move higher again after reversing at support, IV is likely to come down some. With the current IV at 53.15%, if IV drops 10% down to 43.15%, the premium would drop about 0.50 (0.05 X 10) because of vega. That is about a $50 loss due to vega alone, which is over 21% (0.50/2.33) of the original premium. Without a doubt, some if not all of the loss could be nullified by the stock increasing its premium due to a move higher from the positive delta, but a small move higher might be negated completely.

A Spread Might Help

As I like to say, when in doubt, spread it out. A spread trade that lowers the vega risk might make more sense in the environment described above. Selling an option with negative vega would do that. Knowing how the greeks can affect your option position can be critical to making money in the options market, so know what your exposure is at all times.

John Kmiecik, Market Taker Mentoring