What You May Not Know About Option Delta

In my experience teaching option traders, I would say that option delta is probably one the easier option greeks to get a handle on over time. To me, it seems that option gamma and vega are the most difficult. That said, there are still several facts about delta that many option traders just don’t know or realize. Let’s go through a few together.

Delta is the rate of change of an option based on the underlying. To keep it simple, for every $1 the underlying moves, the option premium should change by the amount of delta. Essentially there are only four things you can do with options: buy a call, sell a call, buy a put and sell a put. Long calls and short puts have positive deltas and can benefit from a move higher in the underlying. Short calls and long puts have negative deltas and can benefit from a move lower in the underlying.

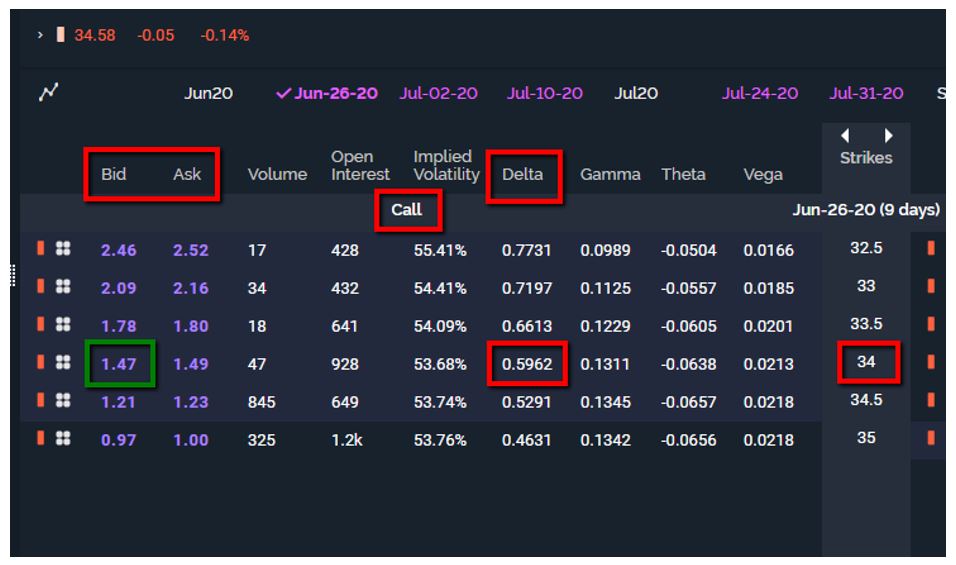

Take a look at the example below. If an option trader bought the 34 strike call, he or she would pay 1.49 (ask price). The position would have a positive delta of 0.60 (rounded up from 0.5962). If the underlying moved $1 higher, the ask premium should increase to 2.09 (1.49 + 0.60) based solely on the delta.

If you have on more than one position at a time for the same strategy, you need to total up the deltas. If your positive delta total is bigger than your negative delta, a move higher will benefit the position whether it is a debit or credit spread. If your negative delta total is bigger than your positive delta, a move lower will benefit the position. Simple and easy to remember.

The last thing that has helped me and many others as far as delta goes is knowing how the premium and deltas will change. I like to say calls and puts will react the same way depending on the underlying. What I mean is that call option premiums will always increase (keeping everything else constant), as will the deltas, if the underlying rises and vice-versa. Put option premiums as well as the deltas will always increase if the underlying falls and vice-versa. Many option traders get confused on what is positive and what is negative, and to me this is an easy way to remember how the premium and delta will change. Obviously, whether you benefit from the move just depends on if you are positive or negative delta.

Take a look at the option chain from above again. What if this time, an option trader sold the 34 strike call for a premium of 1.47 (bid price)? Now the position has a negative delta of 0.60 (rounded up again) because of the short call position. But if the underlying moved $1 higher, the call premium would still increase because call option premiums increase when the underlying rises, all else being held constant. In this case the premium would increase to 2.07 (1.47 + 0.60).

There is so much more to delta than what we’ve covered here, but these key points can help you understand delta much better. As always, getting a proper education can only improve your odds for potential success as an option trader.

John Kmiecik, Market Taker Mentoring