Don't Forget to Add Up Option Greeks

Understanding the option greeks is completely critical to an option trader. Knowing what greeks are, positive or negative, and how changes will affect your position is essential. That said, many option traders I talk to (just this past week, in fact) forget that the greeks do add up the bigger the contract size is.

What Drives the Trade

I love to tell my student option traders to think of the option greeks like the gauges in your car. They give you an idea of how the trade should adjust (profit and loss) based on how the underlying moves, time passes and volatility changes, to name a few factors. But one thing about the greeks that is often overlooked is how they multiply based on contract size.

Greeks Multiply

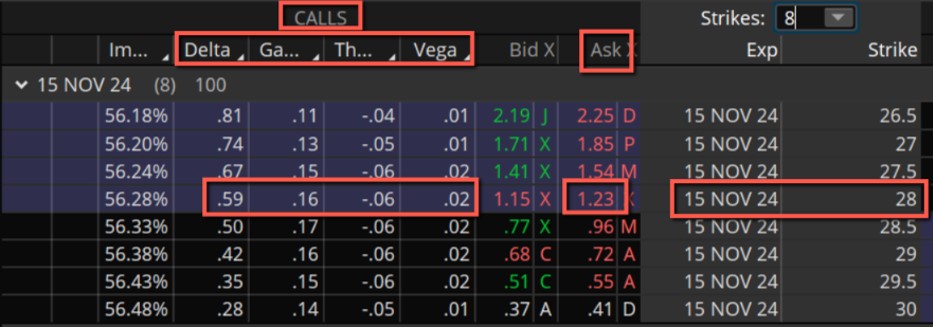

Let’s take a look at an example using the option chain below. Say an option trader buys 1 contract of the November 28 calls because he or she is bullish on the stock.

The current delta is approximately 0.59 ($59 in real terms), which means for every move of $1 on the stock, the option premium should change by that amount. Gamma would change delta by approximately 0.16 for every $1 change. One day of time passing would reduce the call premium by about $0.06 ($6 in real terms) based on the theta, and a 1% change in implied volatility would increase or decrease the option premium by about $0.02 ($2 in real terms) based on the current vega.

More Than One Contract

But what if a trader purchased 5 contracts? Now an option trader needs to consider that all the greeks get multiplied by 5 for the overall position. A $1 move higher based on delta alone (keeping gamma constant at this point) would increase the premium by $2.95 (0.59 X 5) or $295 in real dollars. That is great if the stock rallies, but an option trader needs to understand how the risk multiplies if the stock declines as well. Losses can grow in a hurry so it is vitally important to understand not only what the gains would be but also the potential for a significant loss.

It's Not Just Delta

Delta is not the only option Greek that will multiple like rabbits. Three days passing now results in the overall premium for the position dropping $0.18 (0.06 X 3) or $18 in real terms. This multiplication is also true for gamma and vega. So, if an options trader is worried about being exposed in some capacity, he needs to consider position sizing and/or consider a spread that may limit his exposure, which he or she should be doing anyway. Having and understanding this knowledge is key.

Wrapping It Up

Knowing what the option greeks are and how they can affect your position is paramount for an options trader. Just don’t forget that increasing as well as decreasing your position size can also affect your potential profit and loss.

John Kmiecik, Market Taker Mentoring