Keep an Eye on Implied Volatility During Earnings

The market has been very volatile despite generally moving higher, and now the rush of quarterly earnings may increase volatility for many stocks. Implied volatility levels have been really low, but individual IV levels are expected to rise in front of earnings. The definition of implied volatility that I like best is the estimated volatility of the security in the future that is reflected in the price of the option. In essence, it tells an option trader if options are cheap or expensive at the moment. Historical volatility is the volatility of the security based on the past. It is basically how quiet or volatile the stock has performed previously, which is shown on the underlying’s chart.

IV Rises as Earnings Approach

An important thing to keep in mind is that IV will continue to rise for expirations that take place after the earnings announcement as the earnings date get closers. This is particularly true for volatile stocks that have gapped in the past after the announcement. In other words, option prices will increase due to IV levels rising (all other factors being held constant) because there is a significant chance of a reaction to the announcement. For an option trader, it is good to be positive vega (measure of the option’s sensitivity to changes in IV) with an expiration that takes place after the earnings date before the announcement and negative vega over the announcement.

IV Does Not Rise for All Expirations

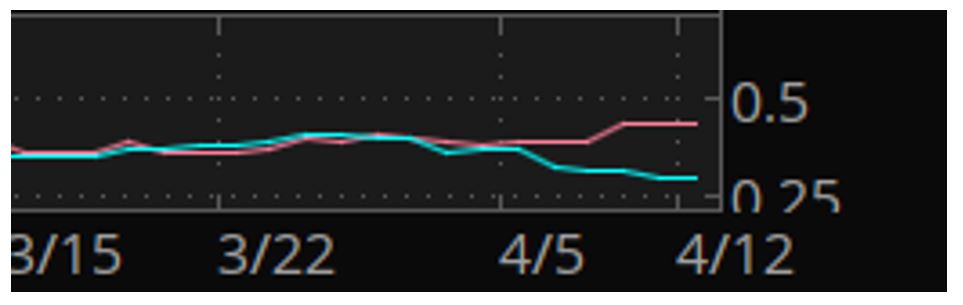

Many option traders will use the 30-day IV and HV. When the earnings date falls within 30 days, the 30-day IV will rise. The IV level will then be above the HV level, which many option traders look for when assessing if IV is high or low. But don’t be fooled. Just because the 30-day IV is above HV it does not mean the expirations that take place before the announcement will be elevated too. Take a look at the two screenshots below. The company was expected to announce on April 20 (within 30 days). The first screenshot shows the 30-day IV (in red) above the 30-day HV (teal).

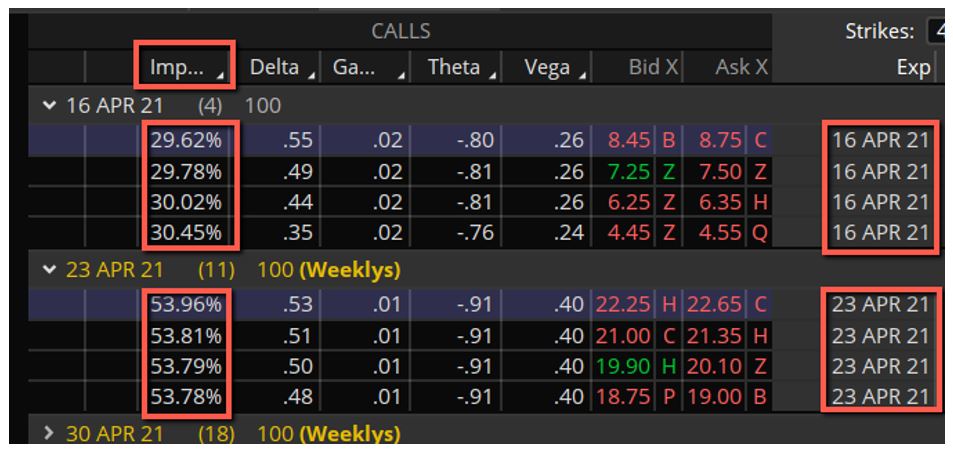

The second (below) shows the IV level much lower for the expiration that takes place prior to the announcement and the expiration right after the announcement. You can see it is quite the skew from where it had been.

After the Announcement

IV levels will decrease after a volatility event like an earnings announcement is over. It may be tempting to hold long positions over the announcement, but just know that option prices will decrease because of the IV dropping afterward. That is why holding a positive vega position over the announcement may not be wise. Many option traders find that out the hard way in they are not well educated about the IV crush. On paper it may seem attractive knowing there is a good chance the stock will gap. But in reality the drop in IV with the subsequent drop in the premium from vega may spoil profitable chances.

These are just a few things to think about as an option trader based on pending earnings. When in doubt or without the proper education, it may be prudent to avoid the announcement altogether. Good luck!

John Kmiecik, Market Taker Mentoring