Does Your Option Delta Make Sense?

By simple definition, option delta is the rate of change of the option premium based on the movement of the underlying. I like to say that delta will change the option premium for every one dollar change in the underlying. This is true of any option strategy and particularly vertical debit spreads like bull calls and bear puts. But many option traders fail to realize that an extremely small positive or negative delta will fail to provide much of a profit change for a small move.

This concern comes up often with my one-on-one option coaching students. They are befuddled that even though the underlying moves in the intended direction, the position is up only a small amount. Some will say it’s because expiration is still far away (which can be partially to blame due to potential positive theta), but many have no clue why. Let’s take a look at an example.

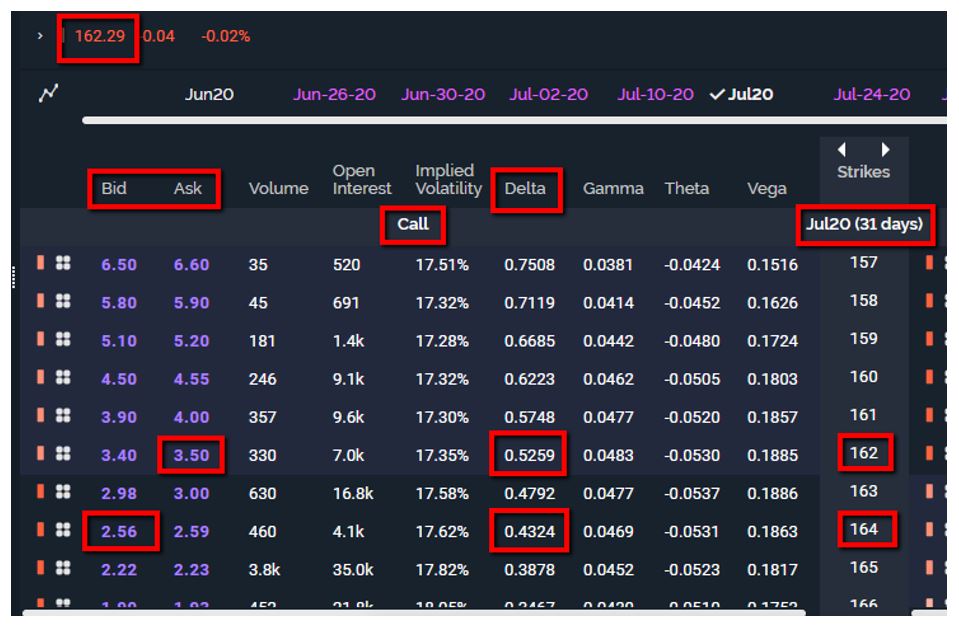

Let’s say you were bullish on this stock shown above and expected it to rise. A bull call spread can be implemented by buying the 162 strike call for 3.50 and selling the 164 strike call for a credit of 2.56. The total cost and risk to the option trader is 0.94 (3.50 – 2.56). But look closer at the delta. It is approximately a +0.09 (0.52 – 0.43) delta. So, if the stock moved higher by $2, the position would only make about 0.18 (2X 0.09) or $18 in real terms. That is probably not the worst scenario you can imagine, but there may be a better way to profit.

Everything in option trading is a trade-off, and this case is no different. To get a bigger positive theta, more risk is necessary. What if the 160/165 bull call was implemented as in the example below?

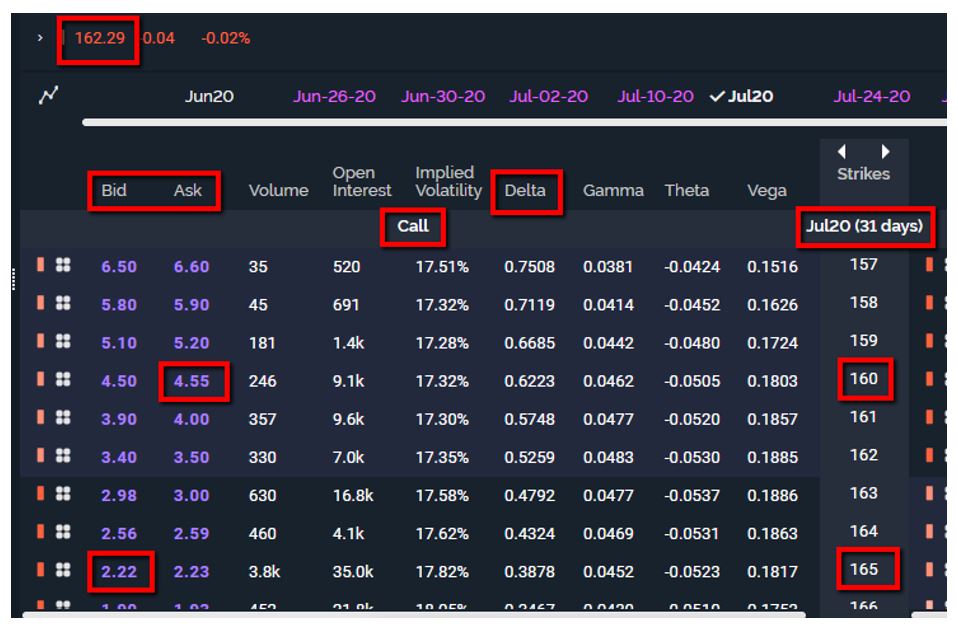

The 160 strike call would be purchased for 4.55 and the 165 call strike would be sold for 2.22. Now the cost and the risk go up to 2.33 (4.55 – 2.22). But the delta increases to +0.23 (0.62 – 0.39). Now a $2 increase will return about 0.46 (2 X 0.23) or $46 in real terms. It is a better return on the investment too.

Clearly there are other factors besides delta that can change the dynamics of the position. But if option traders are cognizant of their delta on the position, it can make them potentially more profitable on directional trades.

John Kmiecik, Market Taker Mentoring